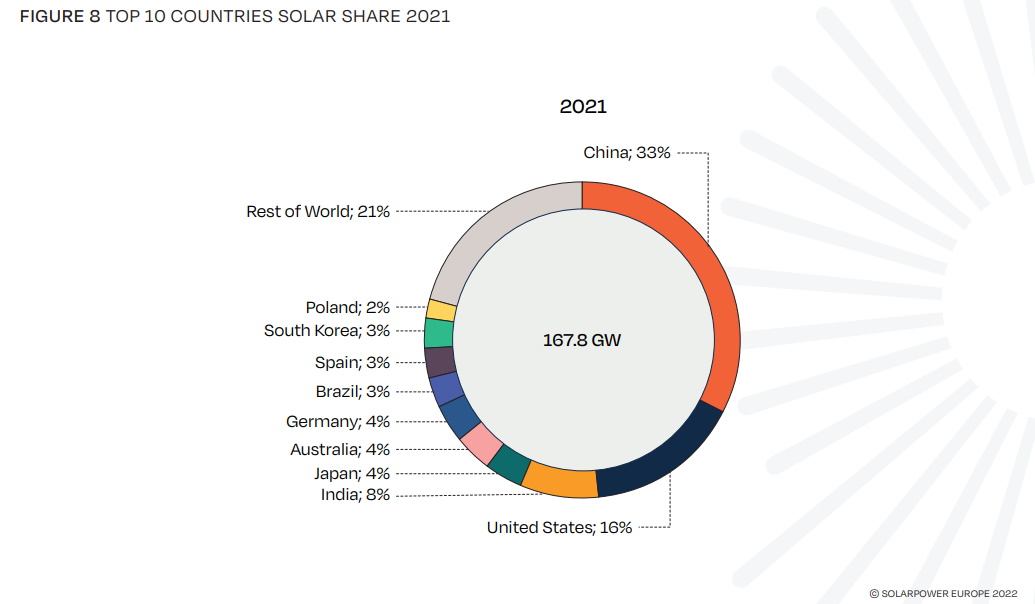

Top 10 solar markets in 2021

China maintained its position as market leader with a 14% annual growth rate and an all-time high of 54.9 GW of new solar capacity. It added twice as much capacity than the second largest market, the United States, and as much as the other top five markets combined.

The US repeated their performance of 2020 presenting a 42% growth rate and 27.3 GW of newly installed capacity in 2021 with 72% of all installations coming from the utility segment.

India regained the third place after a plummeting performance in 2020 preceded by a continuous decline from 2017. With its 265% year-on-year growth rate of 2021, India is back on track to reach its 500 GW target of non-fossil fuel electricity capacity by 2030.

Japan remained in fourth position despite a decrease of 21% in new installations compared to 2020 and is back on the downward path it experienced after a record 2015. New incentive tools are showing success and self-consumption business models are also becoming more attractive.

Australia defended its fifth-place ranking continuing its upward trend in solar market performance that started in 2014 and gaining 18% in 2021. After difficult business conditions in 2020 limited the growth in the industrial and utility-scale segments, strong interest in residential rooftop systems brought the market to a new high.

Germany also maintained its position in sixth place. The grid connections in Europe’s largest solar market grew by 23% compared to 2020. Its proven feed-in premium scheme and regular tenders for systems larger than 750 kW contribute to a stable market, and rooftop installations remained the backbone of Germany’s solar industry.

Brazil, which joined the top 10 in 2020, improved to seventh place but is still the only Latin American country in the group. In 2021, it presented a record growth of 74% compared to 2020 with 5.5 GW installed (after installing 3.2 GW in 2020).

Spain improved its position to rank eighth with an increase of 37% (4.8 GW) of newly installed capacity compared to last year. The strong PPA market without any kind of subsidies is the backbone of the country’s development, probably making it the world’s largest subsidy-free solar market. Abolishing the Sun Tax in early 2020 opened the door for the self-consumption rooftop market, which has now started to grow.

South Korea, in ninth position, showed a 6% solar market slow-down of new installations, but it is still the country’s second-best achievement. The Korean Renewable Portfolio Standards scheme, the market’s main driver, requires utility companies with generation capacities exceeding 500 MW to supply between 6% and 10% of their electricity from new and renewable power sources by 2023 - a programme that includes over 90% of the PV installations in the country.

Poland entered the top 10 with 56% growth compared to 2020 and 3.8 GW installed. Thanks to a favourable net-metering scheme, the driving force has been the small rooftop segment below 50 kW. With the scheme being discontinued in 2022, the future of the small rooftop market is up in the air, but large-scale solar PV projects are gaining attraction as there are no significant regulatory barriers (compared to wind), and they offer the capacity to meet the country’s energy needs in a short timeframe.

Focus: The Latin American solar market

More and more Latin American countries have joined the fight against climate change and have started to actively reduce greenhouse gas emissions to keep global warming below +1.5°. Volatile prices and dependency on energy imports are also reasons why many of them are working towards ensuring local energy security and energy self-sufficiency. The warm climate with abundant sunshine and the falling costs of renewable energy technologies make solar PV an attractive solution. Although renewable energy technology has experienced significant and diversified growth, solar PV dominates thanks to its competitiveness and simplicity and has strong popular and governmental support due to its importance for job creation and economic development.

Beneficial public policies - especially in Brazil, Chile, and Mexico - have also incentivised the employment of rooftop solar PV systems for homes and small business in recent years, whereas other countries with less favourable supporting frameworks and investment conditions are still lagging behind in growth.

Electricity auctions remain a key driver for large-scale solar PV development despite pandemic-induced delays and challenges, but the low volume of contracts recently auctioned by governments has large-scale solar PV market players looking for other options like bilateral PPA (Power Purchase Agreements) in the free electricity market and self-electricity generation by direct ownership or lease of large-scale solar PV power plants. As such, clear targets from governments and regulatory certainty are required.

Other drawbacks in the growth prospects are related to recent disruptions in the international supply chain caused by costs, freight issues, and access to raw materials for solar PV installation components as many Latin American countries depend on imported equipment like modules and inverters that local manufacturing cannot yet provide due to lack of both policy and a qualified workforce.

In the long term, however, continued cost decrease of equipment, improved efficiency of technology, and large-scale fabrication and processing will contribute to the upward trend of solar PV energy in Latin American countries in their fight to reduce climate change and in their transition towards clean and local energy sources.

Download the report to learn more details about development in the region’s different countries and discover a number of large solar plant case studies in Latin America.

The world goes solar: SolarPower Europe's Global Market Outlook for solar power 2022-2026

In this report published at the InterSolar Europe trade fair, SolarPower Europe looks back on the evolution of solar power worldwide over the last two decades and forecasts what is expected over the next four years in this rapidly growing industry. The report includes a special focus on the Latin American market, the latest trends in solar technology, and a thorough analysis of the 17 countries that installed more than 1GW of solar energy in 2021.

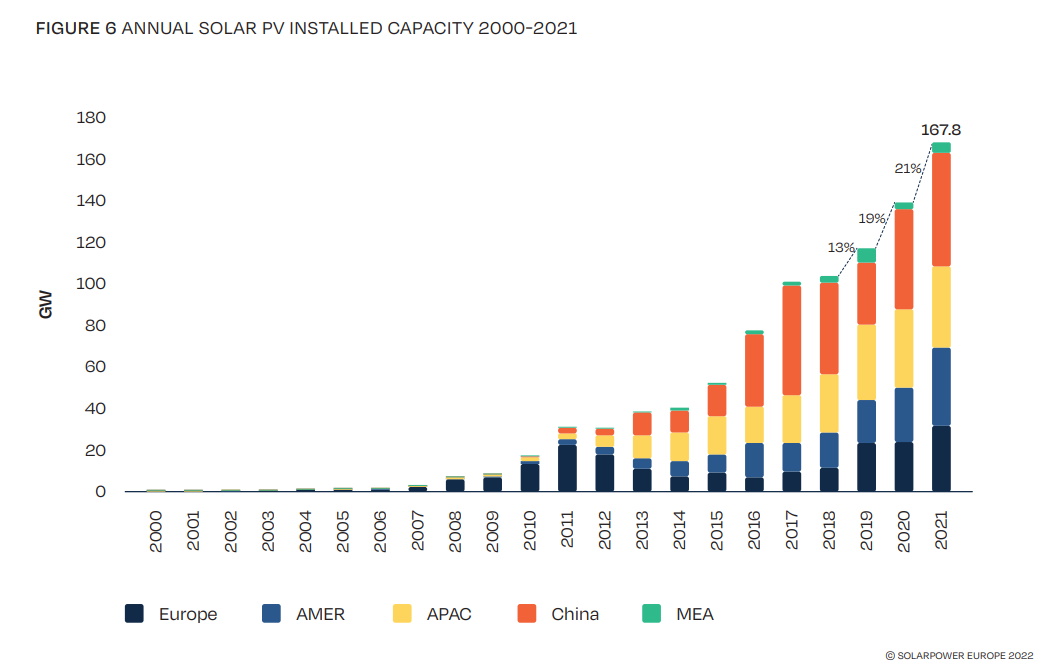

Overall, the industry has reason for celebration: 1 TW of globally installed solar capacity was reached in early May 2022. From just 500 GW installed in 2018, global solar power is set to double in less than four years as SolarPower Europe expects the planet to reach 2 TW by 2025.

{kind=link}

{kind=link}

The journey of solar success from 2000-2021

In early 2002, the cumulative grid-connected solar energy volume had reached 2 GW. 20 years later, it is 500 times that much as the 1 TW threshold was passed in May 2022.

Despite rapid evolution in technology increasing efficiency and reducing costs, policy makers could not keep up with providing proper legal frameworks. Lengthy permission processes are a common reason for the slowing down of major developments.

The reasons for solar’s success over other technologies are diverse, but its steep cost reduction curve over the last decade is the ultimate factor that converted solar into the global cost leader. Compared to 2009, the cost of producing solar power has decreased by 90%. Solar has been cheaper than fossil and nuclear energy for several years now, but in 2021 it even overtook wind energy in terms of cost efficiency in many parts of the world. Depending on the part of the world, a kWh of solar energy costs less than 0.013 USD.

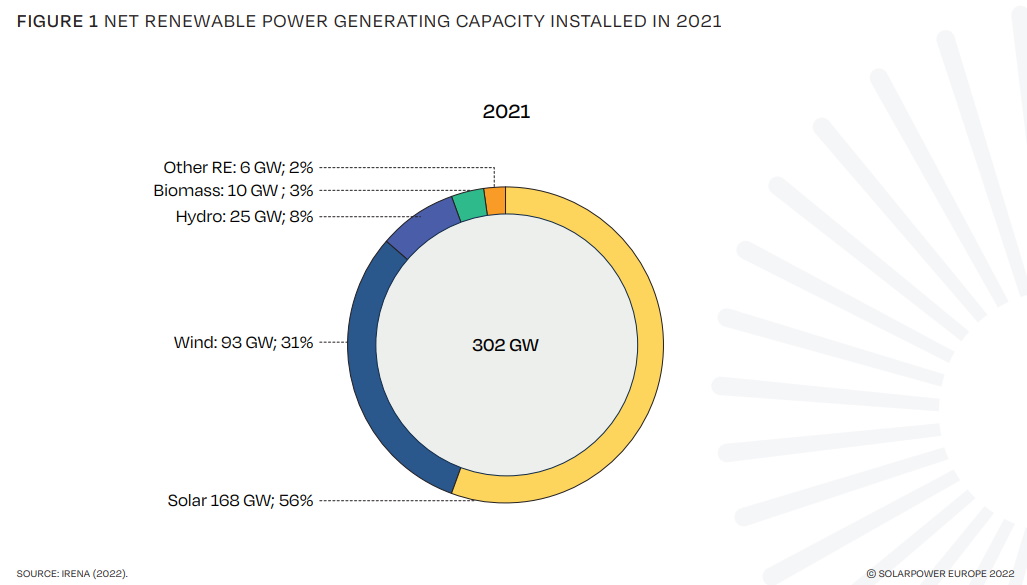

In 2021, solar energy claimed a share of 56% of the over 300 GW of new global renewable power generating capacity created. Looking at the global electricity demand, however, where non-renewable sources dominate with over 70%, solar’s share is small at around 4%.

Looking ahead: 2022–2026

According to SolarPower Europe, the increase in solar component and freight costs affecting the industry in 2021 and extending into 2022 will not slow down growth. Another record-breaking performance is expected with around 36 GW to be installed worldwide in 2022. The next four years will see a strong demand for solar. The threshold of 2 TW is expected to be reached by the end of 2025 with 2.3 TW of solar energy projected to be installed worldwide by the end of 2026.

Despite good growth prospects, in the present inflationary environment prices are expected to remain high until the end of 2022: higher material, component, and transport prices; the war in Ukraine; and the lockdown in China are putting pressure on the global economic situation that had only recently started to recover from the pandemic-induced slowdown.

The report provides more details about the development prospects of solar and its segments (rooftop vs utility-scale) in the world’s different markets.

{kind=link}

SolarPower Europe (2022): Global Market Outlook for Solar Power 2022-2026, May 2022.

About SolarPower Europe:

SolarPower Europe is a link between policymakers and the solar PV value chain with the mission to ensure solar becomes Europe’s leading energy source by 2030. As the member-led association for the European solar PV sector, SolarPower Europe represents over 260 organisations across the entire solar sector.

With solar sitting on the horizon of unprecedented expansion, SolarPower Europe works together with its members to create the right regulatory and business environment to take solar to the next level.

Text:

Constructalia

Images:

© SolarPower Europe

Download the report here

Trends

Solar modules and solar PV systems still consist of the same components, but significant differences can be noted with a closer look: improved materials; new solar cell technologies; and augmented efficiencies of cells, modules, and inverters prove that change has taken place. These transformations affect the entire system design: large wafers and significantly higher module power ratings have led to the optimisation of inverters and mounting systems over the last two years.

In the chapter ‘Trends – What’s cool in solar technology,’ SolarPower Europe summarises the latest solar technology developments in the value chain that have contributed to the industry’s growth and that will continue to do so.

The world’s GW-scale markets

In the last chapter of the report, SolarPower Europe takes a closer look at the GW markets, presenting an analysis of the 17 countries that surpassed 1 GW of solar power installed in 2021 and forecasting their expected performances until 2026.